Page purpose. This is the technical companion to the Spain Wealth Tax Calculator. It documents how the calculator estimates your wealth tax, what data it uses, what is approximated, and what falls outside its scope.

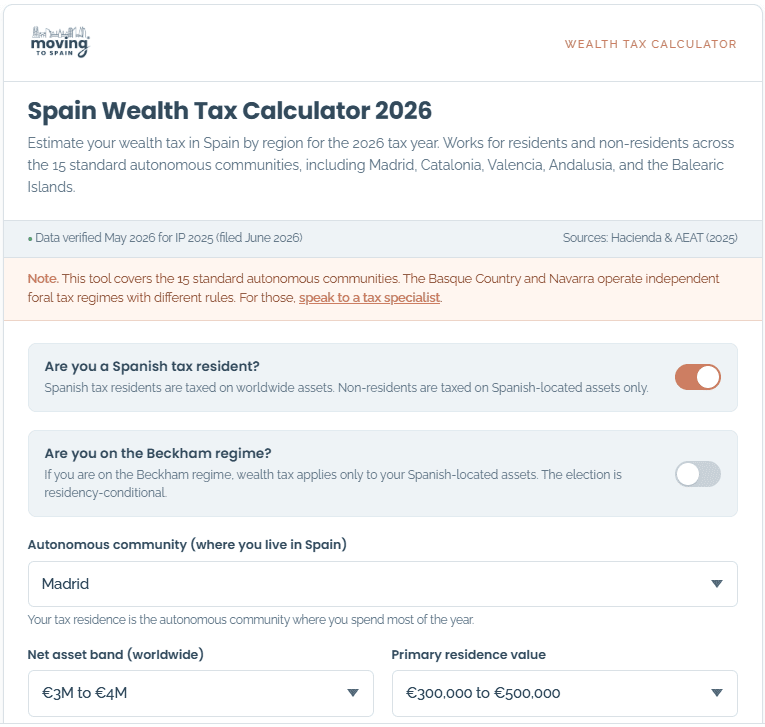

One-line summary. The calculator estimates the combined annual burden of Spain’s regional Wealth Tax (Impuesto sobre el Patrimonio), national Solidarity Tax on Large Fortunes (Impuesto Temporal de Solidaridad de las Grandes Fortunas, ITSGF), and the 60% rule cap, for the 2026 tax year, in any of Spain’s 15 standard autonomous communities, for both Spanish tax residents and non-residents.

What the calculator does

The calculator models three layers of Spanish wealth tax in this order:

1. Regional Wealth Tax. Calculated on net assets above the regional exemption, using either the state scale or the autonomous community’s own scale where one exists. Regional reliefs and 100% relief mechanisms are applied where applicable.

2. National Solidarity Tax (ITSGF). Calculated on net wealth above €3,000,000. The regional Wealth Tax already paid is credited against the Solidarity Tax, so the same wealth is not taxed twice. In regions with 100% relief, no regional Wealth Tax is paid, so the Solidarity Tax captures the equivalent amount.

3. The 60% rule cap. Tests whether your combined income tax and wealth tax exceed 60% of your taxable income. If so, the wealth tax bill is reduced to bring the combined total back to the cap, subject to a minimum 20% of the original wealth tax assessment.

For Spanish tax residents, the calculation is run against worldwide net assets. For non-residents, it is run against Spanish-located assets only.

What the calculator does not do

The calculator does not provide tax advice. It does not file forms, calculate income tax (IRPF) in detail, or model the asset-by-asset valuation rules that determine the exact taxable base for any individual return. It does not cover the Basque Country or Navarre, which operate independent foral tax systems with different rules. It does not calculate Modelo 720 or Modelo 714 filing obligations, but it does note when they likely apply. For your specific case, speak to the Moving to Spain Expert Tax Partner.

Data sources

All rates, brackets, exemptions, and reliefs used in the calculator are drawn from current Spanish government publications:

- Ministerio de Hacienda y Función Pública. Tributación Autonómica. Medidas 2025. (Published April 2026.) This is the consolidated reference for autonomous community wealth tax measures applicable to the 2025 tax year, which is the year filed in June 2026.

- Agencia Tributaria (AEAT). Manual práctico Patrimonio 2025. The official AEAT guide to the wealth tax for the 2025 tax year, including the state scale and the national rules that apply where regions have not set their own.

- Ley 19/1991, de 6 de junio, del Impuesto sobre el Patrimonio. The primary legislation governing the wealth tax in Spain includes Article 31, which establishes the 60% rule.

- Ley 38/2022, de 27 de diciembre. The legislation that introduced the Solidarity Tax (ITSGF) for the 2022 tax year.

- Real Decreto-ley 8/2023, de 27 de diciembre. The legislation that extended the Solidarity Tax beyond its original sunset and converted it to an indefinite measure from IP 2024 onwards.

- Tribunal Supremo, Sala Tercera. Rulings ECLI:ES:TS:2025:4849 (29 October 2025) and ECLI:ES:TS:2025:4846 (3 November 2025), which extended the 60% rule to non-resident taxpayers on free-movement-of-capital grounds.

- Tribunal Económico-Administrativo Central (TEAC). Resolution 00/02959/2023/00/00 of 24 September 2025, which confirmed that non-EU residents may elect the autonomous community rules where the bulk of their Spanish assets are located.

The full data set used in the calculator has been audited against these sources by the Moving to Spain Expert Tax Partner and is reviewed at least annually.

Data stamp. Calculator data verified May 2026 for the IP 2025 tax year (filed June 2026).

The state scale

Spain’s national wealth tax scale applies by default where an autonomous community has not set its own. Following Ley 11/2020 (Presupuestos Generales del Estado 2021), the top bracket has been 3.50% since IP 2021.

| Taxable base from | Taxable base to | Marginal rate |

|---|---|---|

| €0 | €167,129.45 | 0.20% |

| €167,129.45 | €334,252.88 | 0.30% |

| €334,252.88 | €668,499.75 | 0.50% |

| €668,499.75 | €1,336,999.51 | 0.90% |

| €1,336,999.51 | €2,673,999.01 | 1.30% |

| €2,673,999.01 | €5,347,998.03 | 1.70% |

| €5,347,998.03 | €10,695,996.06 | 2.10% |

| €10,695,996.06 | Above | 3.50% |

This is the scale applied to Asturias, Aragón, Cantabria (before relief), Castile and León, Castilla-La Mancha, Canary Islands, Extremadura (before relief), La Rioja (before relief), Madrid (before relief), Murcia (before relief), and the Balearic Islands. Catalonia and Valencia use their own scales that closely track the state scale across most wealth levels but diverge in the top brackets.

Regional treatments

The calculator applies the following region-specific rules, all of which are verified against the Tributación Autonómica 2025 publication. Each region’s treatment has been confirmed by the Moving to Spain Expert Tax Partner.

| Region | Personal exemption | Scale | Relief mechanism |

|---|---|---|---|

| Andalusia | €700,000 | State | 100% relief on regional quota, structured as ITSGF-linked carve-out |

| Aragón | €700,000 | State | None |

| Asturias | €700,000 | State | None |

| Balearic Islands | €3,000,000 | State (regional) | Raised exemption to €3M from 2024 (not a relief; a raised exemption) |

| Canary Islands | €700,000 | State | None |

| Cantabria | €700,000 | State | 100% relief on regional quota |

| Castile and León | €700,000 | State | None (the 100% relief that previously existed was repealed in 2011) |

| Castilla-La Mancha | €700,000 | State | None |

| Catalonia | €500,000 | Catalan scale (own scale with top bracket at 3.48% above €20M while ITSGF is in force) | None |

| Extremadura | €500,000 | State | 100% relief on regional quota |

| Galicia | €700,000 | State | 50% relief on the regional quota |

| La Rioja | €700,000 | State | 100% relief on regional quota from IP 2025 |

| Madrid | €700,000 | State | 100% relief on regional quota |

| Murcia | €700,000 | State | 100% relief on regional quota linked to the Solidarity Tax, applicable for IP 2025 onwards (reverted from a one-year €3.7M experiment in IP 2024) |

| Valencia | €1,000,000 | Valencian scale (top bracket 3.5%) | None; exemption raised to €1M from May 2025 |

The Basque Country and Navarre are not included in the calculator because they operate independent foral tax regimes with different rules. For those, speak to the Moving to Spain Expert Tax Partner.

The Solidarity Tax layer

The Solidarity Tax (ITSGF) applies to net assets above €3,000,000, with the same €700,000 personal exemption and €300,000 habitual residence exemption as the regional Wealth Tax. The brackets are:

| Net assets from | Net assets to | Solidarity Tax rate |

|---|---|---|

| €0 | €3,000,000 | 0% |

| €3,000,000 | €5,347,998 | 1.70% |

| €5,347,998 | €10,695,996 | 2.10% |

| €10,695,996 | Above | 3.50% |

The credit mechanism. The Spanish regional Wealth Tax already paid is fully creditable against the Solidarity Tax. This means a resident in a state-scale region with a sizeable wealth tax bill typically owes zero additional Solidarity Tax, because the wealth tax has already absorbed it. A resident in a 100% relief region (Madrid, Andalusia, Cantabria, La Rioja, Extremadura, Murcia) pays no regional Wealth Tax, so the Solidarity Tax captures the full amount.

Why “100% relief” does not mean “no tax above €3M.” The Solidarity Tax was specifically designed to capture revenue from regions that had used 100% relief to eliminate the regional Wealth Tax. Above €3M of net wealth, the national tax produces a similar bill regardless of whether you live in Madrid, Asturias, or anywhere else. The calculator displays this clearly in the per-region breakdown.

The 60% rule

Under Article 31 of Ley 19/1991, the combined burden of wealth tax (regional + Solidarity) and income tax (IRPF) cannot exceed 60% of your taxable IRPF income. If it were, the wealth-tax portion would be reduced until the combined burden reached 60% of income. The reduction is capped at 80% of the original wealth tax assessment, meaning at least 20% of the original assessment is always payable.

The Spanish Supreme Court extended this rule to non-residents in October and November 2025 (rulings ECLI:ES:TS:2025:4849 and ECLI:ES:TS:2025:4846), confirming that any restriction of the cap to residents would breach the free movement of capital under EU law. Non-EU residents, including US, UK, Canadian, and Australian taxpayers, are explicitly covered.

Where the calculator simplifies. Calculating the exact 60% cap requires precise knowledge of your income tax (IRPF) liability. IRPF is itself a complex calculation involving regional surcharges, the type of income (salary, pension, dividend, capital gains are each taxed differently), personal and family circumstances, and deductions. The calculator does not attempt to replicate the full IRPF calculation. Instead, it applies a flat 35% approximation to your taxable income band as a stand-in for IRPF.

Why is this simplification acceptable for an estimator? At the wealth and income levels where the 60% rule matters most (high wealth, modest income), a 35% IRPF approximation typically produces a final wealth tax estimate within ±10% of the precise figure. For the user’s most important question — “is my wealth tax bill going to be five figures or six?” — the simplified calculation answers correctly in almost all cases. For users near the boundary of the 60% rule (where small income differences flip whether the cap engages), the calculator may be off by a meaningful percentage. Anyone in that band should run their numbers with the Moving to Spain Expert Tax Partner, who applies the full IRPF calculation rather than the simplified approximation.

Non-resident treatment

When the “Spanish tax resident” toggle is set to off, the calculator changes its behavior in three ways:

- Asset scope. Only Spanish-located assets are taxed, in line with Article 6 of Ley 19/1991. The user’s asset band is interpreted as net Spanish-located assets, not as worldwide assets.

- Habitual residence exemption. The €300,000 home exemption applies only to residents of Spain who are in their habitual residence there. Non-residents’ Spanish property is, by definition, not their habitual residence, so this exemption does not apply.

- Region election. Per TEAC Resolution 00/02959/2023/00/00 of 24 September 2025, non-EU residents may elect the autonomous community rules where the bulk of their Spanish assets are located. The calculator allows this election by letting the non-resident user pick any of the 15 standard regions.

The Beckham regime toggle is automatically disabled when the non-resident toggle is on, because the Beckham regime is residency-conditional.

The Beckham regime layer

Under the Beckham regime (Régimen Especial para Trabajadores Desplazados, Ley 35/2006, Article 93), eligible inbound movers are taxed only on Spanish-located assets for wealth tax purposes during the regime’s six-year window. The calculator approximates this by assuming a typical inbound mover has minimal Spanish-located wealth, and so outputs approximately €0 when the Beckham toggle is on.

This is an approximation, not a precise calculation. A Beckham regime user who has acquired meaningful Spanish-located assets (a Spanish primary residence, a Spanish investment portfolio, Spanish shares) will owe wealth tax on those assets, and the calculator’s €0 output is not representative of their position. The Beckham regime is also individual, not household, so if only one spouse has elected the regime, each spouse should be modeled separately. The calculator flags both limitations in the user interface and routes the user to the Moving to Spain Expert Tax Partner for a calculation based on their actual asset structure.

Calculation method: banded inputs and the midpoint approach

The calculator uses dropdown bands for asset levels, residence values, and income rather than free-text inputs. This is a deliberate design choice with three reasons:

- Accuracy expectations. A free-text input invites the user to expect a precise answer. The calculator is an estimator, not a tax return. Bands signal honestly that the output is a band, not a single number.

- Privacy. Users are more willing to estimate their wealth within a range than to enter a precise figure into a public web tool.

- Calculation tractability. Banded inputs allow the calculator to use band-midpoint values for the calculation. The midpoint is the most defensible single number for a band; using the bottom would underestimate, and using the top would overestimate.

The output is then displayed as a ±25% band around the midpoint calculation. This range reflects the combined uncertainty introduced by banded inputs, the simplified IRPF approximation, and the assumption that asset structure follows the typical inbound mover profile (predominantly liquid assets, a primary residence, and some investment portfolio). For users whose wealth is concentrated in qualifying business shareholdings, pension rights, or other assets subject to specific valuation rules, the actual figure may fall outside the displayed band.

What is excluded from the asset base

The calculator’s “net assets” input assumes the following are excluded, in line with Articles 4 and 7 of Ley 19/1991:

- Pension rights. US IRAs and 401(k)s, UK SIPPs, defined-benefit pensions, and the state pension component for both countries. These are exempt from the Spanish wealth tax.

- Qualifying business shareholdings. Where the user owns a significant stake in a business, manages it, and derives substantial income from it, the shareholding is exempt under Article 4.8 of the Law.

- Intellectual property rights held by the original author.

The calculator’s helper text reminds users to exclude these from their inputs. If a user includes them anyway, the output will overestimate. For users with significant exposure to these categories, the Moving to Spain Expert Tax Partner can confirm what is and is not in the taxable base.

Couple and household assumptions

Wealth tax in Spain is assessed individually. When the user selects “couple” in the household input, the calculator assumes a 50/50 split of net assets and income between the two spouses, calculates the wealth tax for each spouse as a single applicant, and sums the two figures to display the household total.

This is a simplification that suits most cases and misleads some. Most couples moving to Spain hold joint assets in roughly equal proportion. The 50/50 split assumption is realistic for them. However, in cases where one spouse holds the bulk of the household assets (a pre-marital portfolio, a business interest, an inheritance held individually), the household burden will not be evenly distributed and may be materially higher than the calculator’s “couple” output suggests. The calculator’s UI advises users in this situation to run the calculator as a single applicant on the wealthier spouse’s individual position. For households with complex asset structures, speak to the Moving to Spain Expert Tax Partner.

What the displayed range means

The headline number is shown as a range (for example, “€8,000 to €13,000 per year”) rather than a single figure. The range represents the ±25% band around the calculator’s midpoint estimate.

A specialist consultation should produce a number within or close to the displayed range for the great majority of users. Where the actual figure falls outside the displayed range, the most common causes are:

- Significant qualifying business exposure that the calculator’s exemption logic does not model in detail

- Asymmetric asset distribution between spouses where the user selected “couple.”

- Asset valuation specifics (catastral value for property, average value for accounts) that produce a meaningfully different base from the user’s estimated band

- Income type effects on the 60% rule (salary income, pension income, and capital gains income are each treated differently in the precise calculation)

The calculator’s purpose is to give users a defensible first answer to the question “how much wealth tax will I pay if I move to Spain?” The displayed range is wide enough to absorb the simplifications listed above for typical users. For atypical cases, the calculator flags the limitation in the UI and routes the user to a specialist.

Limitations and what falls outside the scope

The calculator does not cover:

- Basque Country and Navarre. These operate independent foral tax regimes. The 15 standard autonomous communities are covered; the two foral regions are not.

- Modelo 720 and Modelo 714 filing. The calculator does not generate filing obligations or produce a form. It estimates the underlying tax owed; the filing process is separate.

- Tax planning structures. Asset restructuring, holding-company arrangements, treaty positioning, and other planning approaches that can materially change the actual bill are out of scope. The calculator computes the tax based on the user’s existing structure as described.

- Cross-border interaction effects. Double taxation treaties, foreign tax credits, treaty residency tie-breakers, and similar cross-border considerations are out of scope for the calculator and require specialist input.

- Inheritance, gift, and capital gains taxes. The calculator covers wealth tax only. Other Spanish taxes are not modeled.

For any of these, speak to the Moving to Spain Expert Tax Partner.

Review and update cycle

The calculator’s rates, exemptions, and regional treatments are reviewed by the Moving to Spain Expert Tax Partner at least annually, in time for each year’s IP filing season. Material updates between reviews (case law, new regional measures, or rate changes published mid-year) are applied as soon as they are confirmed.

The data stamp shown in the calculator UI indicates the date of the most recent verification. If you spot a figure that looks wrong, or a regional rule that has changed since the last review, please contact us, and we will check it.

Summary

The calculator is an estimator, not a tax return. It applies the current 2026 rules to the regional Wealth Tax, the national Solidarity Tax, and the 60% rule in any of Spain’s 15 standard autonomous communities, for both residents and non-residents. It uses banded inputs and a midpoint calculation, displays output as a ±25% range, and approximates the 60% rule using a simplified IRPF estimate. Where the user’s situation falls outside the calculator’s design assumptions, the UI flags the limitation and routes the user to the Moving to Spain Expert Tax Partner for a precise calculation.