The Wealth Tax in Spain causes many people to rethink their plans, but we have good news. For most people moving to Spain, it isn’t a massive issue and certainly no reason to cross Spain off the list! We’re waiting on confirmation of rates from some Autonomous communities, but as of publication, these are the wealth tax figures for 2026.

“The vast majority of people moving to Spain will pay less than €500 per year in tax, if they pay any tax at all. If you have less than €1,000,000 (net) in assets, own a home in Spain, oor choose to live in one of the regions with 100% rebates (where your net assets are below €3M), then the wealth tax is often just some paperwork!” – Louis Williams, Spanish Tax Specialist

The Spanish government uses your total net global assets to calculate your Spanish tax liability, but the amount you pay varies by region. We’ll explore who is liable, how to calculate your net worth, and how much wealth tax you’ll pay in each region. And remember to set March 31st for Modelo 720 and June 30th for Modelo 714. Explore our guide to learn how the Wealth and Solidarity taxes fit into the Spanish Tax System for Expats.

Spanish Wealth Tax – impuesto sobre el patrimonio

The Patrimonio is an annual tax, commonly referred to as the Spanish Wealth Tax, introduced in 1977 and amended in 1992. It is calculated using the total net value of eligible assets on 31 December each year. The tax is progressive, so the percentage tax increases with the total value of your assets minus associated liabilities. There is a national rate, but some regions apply different tax percentages and thresholds.

Each region applies a deduction, so net worth below the deduction threshold is not taxed. The national deduction is €700,000, but it varies in some autonomous regions, and we’ll cover these in detail later in the article.

Summary of Differences: 2025 vs 2026

| Feature | 2025 Tax Year | 2026 Tax Year |

| Non-Resident Cap | Not Available | Available (60% limit applies) |

| Solidarity Tax | “Temporary Extension” | Indefinite/Permanent |

| Valencia Threshold | €500k (Old) / €1M (Proposed) | €1,000,000 (Confirmed) |

| Reporting Duty | Mandatory if assets >€2M | Mandatory if Spanish assets > €2M or if any Wealth Tax is owed. |

How much tax will you actually pay in Spain?

The answer is very specific to your situation – your income mix, investments, which Spanish region you choose, and the structures available to you. Get clarity from our vetted tax specialists who work with expats like you every day.

An Individual Tax

The tax is applied to individuals. This means that each individual must declare their joint assets, specifying the percentage of ownership they hold. So, if a husband and wife jointly own a house worth €1,000,000, they would each declare 50% of the value (€500,000).

In addition, the deductions are individual. In the example above, the husband and wife could claim standard national wealth tax deductions in Spain of €700,000, plus the €300,000 for the family home. This amounts to €1,000,000 each, for a total of €2,000,000.

Spain Wealth Tax Rates 2026 – National Rates

These rates apply by default unless your autonomous community sets different ones.

| From | To | Percentage |

| – | 167,129 | 0.20% |

| 167,129 | 334,253 | 0.30% |

| 334,253 | 668,500 | 0.50% |

| 668,500 | 1,337,000 | 0.90% |

| 1,337,000 | 2,673,999 | 1.30% |

| 2,673,999 | 5,347,998 | 1.70% |

| 5,347,998 | 10,695,996 | 2.10% |

| 10,695,996 | And Above | 3.50% |

Wealth Tax By Community

Important: Non-Residents: Region Election (2026 Update) A TEAC ruling of 24 September 2025 confirmed that non-EU residents (including US, UK, Canadian, and Australian taxpayers) can elect the wealth tax rules of the autonomous community where the bulk of their Spanish assets are located. Previously, this was restricted to EU/EEA residents. This is a material change for non-resident property owners in 2026. So, now a Mallorca villa owner can elect the Balearic regime, a Marbella villa owner can elect Andalusia, and so on.

| Region | Min Rate | Max Rate | Primary Residence Exemption | 2026 Notes |

| Andalusia | 0.00% | 0.00% | N/A | Effective 0% rate |

| Aragon | 0.20% | 3.50% | €300,000 | No special exemptions or reliefs |

| Asturias | 0.22% | 3.00% | €300,000 | Standard national structure |

| Balearic Islands | 0.28% | 3.45% | €300,000 | Personal exemption raised to €3M from 2024 (not a relief; a raised exemption). Below €3M of net wealth no Wealth Tax applies. Above €3M, the regional scale and Solidarity Tax both engage. |

| Basque Country | Álava 0.20% Bizkaia and Gipuzkoa are a complex formula | Álava 2.50% Bizkaia and Gipuzkoa are a complex formula | Álava and Bizkaia €800,000 Gipuzkoa €700,000 | All three provinces apply a 3.50% top rate above €14.5M. Note: independent Foral tax system. |

| Canary Islands | 0.20% | 3.50% | €300,000 | No additional regional relief |

| Cantabria | 0.00% | 0.00% | N/A | Effective 0% rate |

| Castile and León | 0.20% | 3.50% | €300,000 | State scale applies. The 100% relief that previously existed was repealed in 2011 and has not been reinstated. |

| Castilla-La Mancha | 0.20% | 3.00% | €300,000 | No special deductions or regional reliefs |

| Catalonia | 0.21% | 3.48% | €500,000 | Lower personal exemption (€500k) and own scale, with a top bracket above €20M at 3.48% while the Solidarity Tax is in force. |

| Extremadura | 0.00% | 0.00% | N/A | Effective 0% rate |

| Galicia | 0.20% | 3.50% | €300,000 | 50% regional relief on the quota. Above €3M of net wealth, the Solidarity Tax interacts with the relief. |

| La Rioja | 0.20% | 3.50% | €300,000 | 100% relief on the regional quota from 2025. Above €3M of net wealth, the Solidarity Tax applies and captures the equivalent amount. |

| Madrid | 0.00% | 0.00% | N/A | Effective 0% rate |

| Murcia | 0.24% | 3.00% | €300,000 | Reverted to the standard €700,000 exemption for IP 2025 (after a one-year €3.7M experiment in IP 2024). Now applies a 100% relief linked to the Solidarity Tax: effectively zero regional Wealth Tax below €3M. |

| Navarre | 0.16% | 1.04% | €250,000 | €550,000 personal exemption. Note: independent Foral tax system. |

| Valencian Community | 0.25% | 3.5% | €300,000 | Personal exemption raised to €1,000,000 from May 2025. Above that, regional scale applies with a top bracket at 3.5%. |

Note: Six autonomous communities apply a 100% relief, eliminating the regional Wealth Tax for most residents: Madrid, Andalusia, Cantabria, Extremadura, La Rioja, and Murcia. The Balearic Islands also impose a zero Wealth Tax on net assets below €3M by raising the personal exemption. For net wealth above €3M in any of these regions, the national Solidarity Tax applies and captures the equivalent amount.

To get clarity on how this affects you personally, get in touch with our vetted tax specialist.

Who Pays Wealth Tax in Spain?

Your region’s wealth tax policy will dictate how and if you are liable for this tax. You should consult a Spanish taxation expert to ensure compliance with your regional requirements.

In general:

- Spanish Tax (Fiscal) Residents calculate Wealth Tax on their global net worth.

- Non-residents for tax purposes calculate Wealth Tax only on Spanish assets.

Important: The Beckham Law in Spain means that you don’t have to pay Wealth Tax – find out if you qualify.

Wealth Tax Deductions – 2026

A national deduction schedule exists, but regional variations also occur. Federal deductions will apply if a region has not set a local deduction.

National Wealth Tax in Spain: Deductions

- Individual deduction: €700,000

- Family Home in Spain: €300,000

- Any wealth tax paid in a country with a Spanish Taxation Treaty (DTT).

Regional Wealth Tax in Spain: Deductions

Each autonomous region can apply different deductions and levels to the national wealth tax. These override those set nationally. Here are three examples of variations.

- In Cataluña, the individual deduction is lower at €500,000. However, the family home deduction is higher at €500,000.

- In 2025, the Valencian community government increased the individual deduction to €1m and the primary residence deduction to €300K; these rates apply for the 2026 tax year.

- Some regions in Spain allow deductions related to your professional activities.

- Six regions apply a 100% relief on the regional Wealth Tax: Madrid, Andalusia, Cantabria, La Rioja, Extremadura, and Murcia. The Balearic Islands also impose no Wealth Tax on net assets below €3M through a raised personal exemption. You may still need to submit your declaration even if you owe nothing.

These variations make it vital to consult a qualified tax lawyer to ensure you file correctly. They’ll help you to claim all available deductions to minimize the tax you pay.

Included Assets For Your Wealth Tax

You calculate your total net worth as of December 31 each year. This means that something purchased after January 1 and sold before December 31 of the same year will not be subject to wealth tax.

Remember: The calculation is based on net assets, so associated liabilities, such as mortgages or loans, are deducted from the asset values.

- Real Estate (including your primary residence).

- Vehicles (including cars, boats, and airplanes).

- Investments, shares, bank accounts, and savings.

- Business assets (in some cases).

- Jewelry (in some cases).

- Art (in some cases).

Excluded Assets / Exceptions

There are assets that the Spanish government excludes from the Wealth Tax assessment.

- Household Contents (apart from those in the list above)

- A business that

- You own a significant shareholding in

- You manage, and

- Pays a significant part of your net income.

- Pension rights.

- Business assets (in some cases).

- Jewelry (in some cases).

- Art (in some cases).

- Intellectual property rights.

Note: US Social Security and UK state pensions are exempt from the wealth tax, but both are still liable for Spanish income tax once you’re a resident — see our full guide to how Spain taxes US Social Security and foreign pensions.

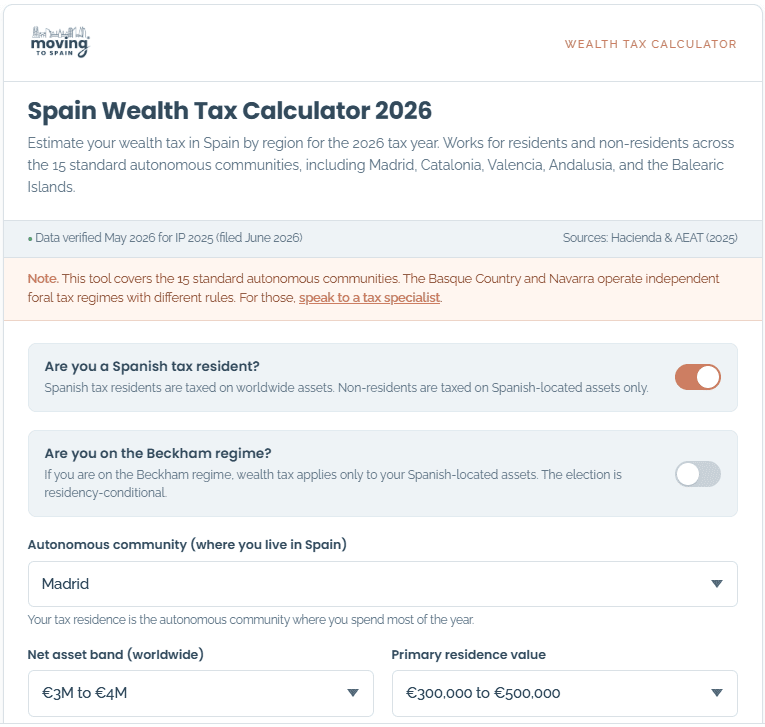

Spain Wealth Tax Calculator 2026

Wealth Tax Calculator

Wealth Tax Calculator

Spain Wealth Tax Calculator 2026

Estimate your wealth tax in Spain by region for the 2026 tax year. Works for residents and non-residents across the 15 standard autonomous communities, including Madrid, Catalonia, Valencia, Andalusia, and the Balearic Islands.

How wealth tax in Spain varies by region

These estimates are based on banded inputs. Your actual figure depends on the specific composition of your assets, qualifying exemptions, and treaty positioning.

Speak to a tax specialistRead More >> Compare All of Spain's Taxes by Autonomous Region

Spain Wealth Tax Worked Examples

You can calculate your wealth tax liability using this formula.

(Total Net Assets - Total Deductions) * Wealth Tax Percentage.

So, you'll pay zero tax if your deductions or allowance exceed your assets.

Example 1: A couple, Sue and Tim, is using the standard national rates and deductions.

| Assets | Asset value | Sue % | Sue | Tim % | Tim |

| Family Home | 1,000,000 | 50% | 500,000 | 50% | 500,000 |

| Joint Shares | 600,000 | 50% | 300,000 | 50% | 300,000 |

| Sue's Boat | 500,000 | 100% | 500,000 | 0% | - |

| Tim's Tiara | 100,000 | - | - | 100% | 100,000 |

| Total Assets | 2,200,000 | 1,300,000 | 900,000 | ||

| Deduction - Individual | 700,000 | 700,000 | |||

| Deduction - Home | 300,000 | 300,000 | |||

| Total Deductions | 1,000,000 | 1,000,000 | |||

| Taxable Amount (Assets - Deductions) | 300,000 | 0 |

So, the tax Sue has to pay is the Autonomous Community rate multiplied by the Taxable amount. Here are four examples.

| Region | Annual Wealth Tax Payable | Notes |

| Asturias | €730 | National Scales Apply |

| Catalonia | €210 | Higher Primary Housing Allowance |

| Madrid | €0 | 100% Relief |

| Navarra | €595 | Lower Tax Scale |

| Valencia | €0 | Higher Personal Allowance |

Example 2:

High-Wealth Worked Example: Sue at €3.5M Taxable Assets

The earlier example shows Sue with €300,000 in taxable assets — a relatively low net wealth tax case. To show how the calculation changes for higher-wealth movers, here's Sue revisited with individual taxable assets of €3,500,000 (net assets of roughly €4,500,000 before deductions) and €50,000 of annual pension income.

This example demonstrates three things the smaller case cannot:

- How the Solidarity Tax engages above €3,000,000 of net wealth.

- How 100% relief regions still produce tax liabilities at this wealth level.

- How the 60% rule caps the bill when income is modest relative to wealth.

| Region | Regional Wealth Tax | Solidarity Tax | Pre-60%-rule total | After 60% rule (€50k income) |

| Asturias (state scale) | €39,946 | €0 | €39,946 | €12,500 |

| Catalonia (own scale) | €39,946 | €0 | €39,946 | €12,500 |

| Valencia (€1M exemption) | €34,846 | €0 | €34,846 | €12,500 |

| Madrid (100% regional relief) | €0 | €8,500 | €8,500 | €8,500 |

| Balearic Islands (€3M raised exemption) | €7,290 | €1,210 | €8,500 | €8,500 |

Three regions converge to €12,500 after the 60% rule fires. Asturias, Catalonia, and Valencia each produce a pre-cap bill in the €35,000 to €40,000 range. The 60% rule then reduces this to the 20% floor of the original assessment, because Sue's combined income tax and wealth tax would otherwise exceed 60% of her €50,000 income. The 60% rule is the most powerful lever available to high-wealth retirees with modest income.

Madrid and the Balearic Islands both produce €8,500, by different routes. Madrid pays no regional Wealth Tax (100% relief), but the Solidarity Tax captures the equivalent amount above €3M. The Balearic Islands raised the personal exemption to €3M, so the regional Wealth Tax base is small (€1.2M after the exemption and the €300k home deduction), but the Solidarity Tax still engages on the €500,000 above the €3M Solidarity threshold. Both regions reach the same total through different mechanisms.

Key insight for high-wealth inbound movers. Above €3M of net wealth, no region produces a zero outcome. The Solidarity Tax is national and applies regardless of where you live. What changes across regions is the mix of the regional Wealth Tax and the Solidarity Tax, not the total burden when income is low. The 60% rule is often the more important lever than region choice, and it depends on your income structure rather than your location. If Sue's income were higher (say €200,000), the 60% rule would not apply in any region, and the regional choice would matter substantially: roughly a €30,000-€40,000 swing between the lowest-burden and highest-burden regions.

This is exactly the kind of analysis a tax specialist will do for your specific case. The interaction between region, asset level, income, and the 60% rule is where most of the tax planning happens. Speak to our tax specialist for a calculation built on your real numbers.

How to File Modelo 720 and 714

There are two forms (modelos) you'll need to know:

Modelo 720

The Modelo 720 is for declaring assets outside of Spain. You'll need to file this form if you have assets exceeding €50,000 globally. You should submit the form annually if the values change by more than €20,000 (total or per item).

If you fall into one of the following three groups, you will need to file one:

- If you have bank savings and deposit accounts held abroad, the sum of all the accounts together exceeds €50,000.

- You have other assets and private pensions held abroad that exceed €50,000. This includes stocks and shares, bonds, life insurance, pension plans, and annuities that are currently being paid. You are in this category if you had a total or surrender value of € 50,000 or more on December 31st of the previous year.

- You own a property with a purchase value of over €50,000, including private property or business premises.

Each individual must submit a report, declare the total value, and share, if the assets are in joint names.

Important: You won't necessarily pay any wealth tax on your assets if your declaration is under the limit. The declaration was implemented to prevent money laundering and fiscal fraud. However, you may be fined if you fail to file it. The fine for failing to file your declaration can be as high as €10,000.

Deadline: 31 March of each year.

Remember: This is an individual tax, so joint owners must each submit a form declaring their percentage ownership of the asset.

How to submit your Modelo 720

The easy way is to have a Spanish tax expert check and file on your behalf. However, you can also file automatically through the Agencia Tributaria website using a Spanish digital certificate.

Modelo 714

Modelo 714 is used to declare Spanish assets. Two groups need to submit this form:

- Those with Spanish assets worth more than €2,000,000.

- Anyone liable for a Spanish Wealth Tax payment.

Deadline: 30 June of each year.

Remember: This is an individual tax, so joint owners must each submit a form declaring their percentage ownership of the asset.

The 60% Rule - Pay Less Tax

One of the biggest tax changes for the 2026 tax year has been settled by the Spanish Supreme Court. Two rulings on 29 October 2025 (ECLI:ES:TS:2025:4849) and 3 November 2025 (ECLI:ES:TS:2025:4846) confirmed that the 60% rule now applies to both Spanish tax residents and non-residents on free-movement-of-capital grounds. Non-EU residents (including US, UK, Canadian, and Australian taxpayers) are explicitly covered.

The total amount of cumulative wealth tax and income tax you pay in a single year has an upper limit. The amount must be no more than 60% of your taxable income.

Impact: If you are a resident or non-resident with high-value Spanish assets but relatively low global income, your Spanish wealth tax bill could be reduced by up to 80%. For example, a retiree with €4M in assets and €30,000 of income might see their wealth tax drop to the 20% floor of the assessment under the 60% rule.

A good tax advisor helps you understand how to manage your investments and income tax for the 60% rule.

Note: The minimum wealth tax amount you'll pay is 20% of the assessment, even if the 60% rule drops you below this figure.

Solidarity Tax

The Spanish Ministry of Finance introduced the 'impuesto de solidaridad a las grandes fortunas' (Solidarity Tax on Large Fortunes) for the tax year 2022 as a temporary measure. It has been extended each year since, and as of IP 2025, it is effectively permanent. It applies to individuals with net assets over €3,000,000 (after deductions). For Spanish tax residents, this means worldwide assets. For non-residents, only Spanish-located assets.

Important: Above €3M of net assets, both the regional Wealth Tax and the Solidarity Tax can apply. The regional Wealth Tax you pay is credited against the Solidarity Tax, so you are not taxed twice on the same wealth. In 100% relief regions (Madrid, Andalusia, Cantabria, La Rioja, Extremadura, and Murcia), no regional Wealth Tax is paid, so the Solidarity Tax captures the full amount above €3M.

The tax is progressive, so the percentage payable increases with the asset value. Estimates are that the Solidarity Tax will impact around 0.1% of Spanish taxpayers.

The government offers deductions similar to those for the wealth tax. Everyone receives a €700,000 deduction, plus an additional €300,000 for a primary home in Spain. Other deductions, including qualifying business, may be available. This means that, for most people, a minimum net asset value of €4,000,000 is required to incur a Solidarity Tax liability.

So, the Solidarity Tax rates (after deductions) are as follows:

| From | To | Tax Rate |

| - | € 3,000,000 | 0% |

| € 3,000,001 | € 5,347,998 | 1.7% |

| € 5,347,999 | € 10,695,996 | 2.1% |

| € 10,695,997 | Upward | 3.5% |

The Spanish government has made this tax permanent, and it is now enforceable.

Note: Unlike the regular wealth tax, which varies by autonomous region, this tax applies uniformly across all 15 Autonomous Communities of Spain with standard taxation regimes, including regions such as Madrid and Andalusia, which offer a 0% wealth tax. There are two Autonomous Community exceptions: the Basque Country and Navarra regions operate under their own unique tax agreements with the Spanish central government, known as the "concierto económico" and "convenio económico," respectively. Navarra and the Basque Country have negotiated "foral" tax systems. We recommend consulting a Spanish taxation expert to understand how you'd be impacted in these areas.

Need Help With Your Wealth Tax?

This is a complicated tax with many variables. The inclusions, deductions, 60% rule, and autonomous regional variations make calculating what you'll owe complex. For this reason, we recommend speaking to a good Spanish Tax advisor. They'll understand how to minimize the amount and pain of the Wealth Tax in Spain.

FAQ - Wealth Tax in Spain

How much is the wealth tax in Spain?

The Spanish Wealth tax is progressive, and the amount you pay depends on several factors. These factors include where you live in Spain, your net assets, and the deductions to which you are eligible.

Where in Spain is there no wealth tax?

Six autonomous communities offer 100% relief, eliminating the regional Wealth Tax for most residents: Madrid, Andalusia, Cantabria, La Rioja, Extremadura, and Murcia. The Balearic Islands also levy no Wealth Tax on net assets below €3M through a raised personal exemption. For net assets above €3M in any of these regions, the national Solidarity Tax applies and captures the equivalent amount.

Will Spain abolish wealth tax?

The tax was introduced as a temporary measure in 1997. It has been abolished and reinstated over the last 25 years. There are constant rumors that the government will repeal it, but there is no end in sight yet.

Do you have to pay wealth tax in Spain every year?

Yes, if you meet the threshold, you'll have to pay tax on your global assets each year. There are significant deductions available, and tax rates vary across Spain's Autonomous Communities.

What assets are exempt from the Spanish wealth tax?

Household goods, pension rights, intellectual property, and some businesses are exempt from wealth tax in Spain. If you have a mortgage, it is offset against the property's value.

What is the Solidarity Tax in Spain?

The Solidarity tax is a progressive tax on worldwide assets exceeding €3,000,000. Many people will be able to claim a €1,000,000 deduction; therefore, Spanish tax residents with assets exceeding €4,000,000 are primarily affected. Solidarity tax rates range from 1.7% to 3.5%. The Spanish government initially introduced this tax as a temporary measure, but it has since become permanent.

What is the Modelo 720 for Wealth Tax in Spain?

The Modelo 720 is a declaration form for Spanish residents to report any overseas assets they hold worth more than €50,000. You must submit the Modelo 720 to the Spanish Tax Agency (Agencia Tributaria) by March 31 each year (detailing the assets you held in the prior calendar year). 'Modelo' is the Spanish word for 'form. '

If I live in Barcelona now and move to Malaga in the future, what will happen to the wealth tax?

For example, if I live in Barcelona in 2023 and own 1.2 million euros in asset worldwide, including deposits, stocks and real estate, I will not need to pay wealth tax when I move to Malaga in 2024. So when will I not need to pay wealth tax for Barcelona?

Do I need to modify my residence information at the Malaga Tax Office, or are there any other procedures required for avoid the wealth tax? Thanks a lot

Hi. I referred this question to our Spanish tax expert partner.

1. If someone moves from Barcelona to Malaga during the Tax year, which tax rates apply for taxes like Wealth Tax? – Where you are empadronado for the majority of the tax year, you will typically pay tax ates for that area.

2. Is the padron sufficient to show that you have moved? – You need to have a new empadronamiento and separately notify your address to the Agencia Tributaria

Hi

I’m an odd one. Empadronado in Canarias but still with UK fiscal residence and company director there with high income and €4 m + world assets.

Am I better with. filing a 72o in Spain? Or stay put in the Uk and my existing status?

Thanks

Hi Harry – I can only answer with more detailed information. I suggest meeting with our cross-border taxation specialist or financial planning partner. All the best, Alastair

If we have a GV property in one spouse’s name, for €500,000, is the deduction only €300? And if so, can the personal €700,000 count towards that? Meaning if all other assets plus the remaining €200,000 from the home are under €1,000,000, would we be exempt from the wealth tax?

Hi Derek. I can give specific tax advice as I am not a qualified Spanish tax advisor. However, in general, the owner of the property will have the €700K personal plus €300K home deduction, so a €1,000,000 total deduction, while the non-owner partner will have the €700K personal deduction. So they’ll have a combined €1,700,000 in total. Our tax partner will be able to assess your case and help you plan the most effective way to meet our obligations. All the best, Alastair

If I have 20 mln euro, so above 10 mln euro (for simplicity don’t mention deductions) I will pay 2,5% Nationality and 3,5% Solidarity ? I was thinking about Spain, but it seems irrational to live there as rich person.

Hi Mike. The low cost of living, lifestyle, and public services make Spain a compelling choice for many high-net-worth individuals. However, the tax bill is unarguably higher than in the USA and other options. Remember that the Wealth Tax is 0% in some parts of Spain. A chat with our wealth management partners can give you an excellent picture of managing a move and other options in Europe to minimize your taxation impact. All the best, Alastair

When calculating Assets to br used in determining if someone must pay the Wealth Tax in Andalucia..do we include any accts we will be the beneficiary of? In other words does my husband need to include my 401k retirement acct if he will be the beneficiary of it upon my passing? Thank you! Eve Jarrett

Hi Eve. While I cannot give specific taxation or financial advice, in general, Spanish residents only need to declare assets they own at the time of the declaration on your Modelo 720. Please get qualified Spanish tax advice for your specific situation. All the best, Alastair

In your Tim and Sue example, shouldn’t the total taxable amount be 200,000 (not 300,000)?

Hi Eric – the example is correct. Spain’s wealth tax is an individual tax and so Sue owes €300,000 and Tim owes €0 (if it were a joint tax then, yes, they would cumulatively owe €200,000). Thanks, Alastair

Hello,

This article is very helpful but I don’t see any mentioning of the Canary Islands. Is there a wealth tax relief like in Madrid? If not, what are the values for your table “Communities with different wealth tax rates and thresholds?”

Gracias,

J

Hi Jeanne – I’ve checked with our cross-border taxation specialist, and currently, the Canary Islands apply the standard federal wealth tax rates. All the best, Alastair

Thank you for posting this information. It is helpful.

Questions:

1. For investments (ex: stocks), do I only value them as of the end of the calendar year or is their value calculated as an average? Not specific to investments, I read that bank accounts are valued at the greater of the end of year value and the last quarter average. So if my investments lose money, the value at the end of the year might be less than the average of the last quarter.

2. For how many years into the future can I use the purchase price of the home to calculate the actual homeowner’s allowance? Just the one? And then do I need to revert to the catastral value? From what I understand, 300,000 Euro is the maximum allowance and the actual allowance is calculated as the maximum of either the purchase price or the catastral value (or another administratively imposed alternative to that). An example from what I understand: if I just purchased my home for 270,000 Euro and its catastral value is 100,000 Euro then I would use 270,000 Euro as my allowance.

Hi Chris. All information we provide is general guidance (as we are not qualified tax accountants), so we can’t give individual advice. Our Spanish taxation specialist will be able to assist with your estimate. All the best, Alastair

Please provide more information about the pension rights exclusion. For example, would an U.S. IRA or 401k be excluded ?

Hi Dave – it would be best to chat with a qualified cross-border taxation specialist in Spain to understand your specific liabilities. All the best, Alastair

Hello Mr. Johnson,

Two questions. 1) A retired couple from the USA rents a villa for almost 3 months every spring and then again for almost 3 months in autumn in Menorca and do not need a visa because they do not violate the 90/180 day Schengen Area rules. They are retired and do not work nor earn any Spanish income. Are they subject to the Spanish wealth tax? 2) A retired couple with US citizenship secure a Spanish Non-Lucrative Visa and rent a villa every year in Menorca for 8-10 months. They have no Spanish assets (no car, no home, no Spanish bank account, no Spanish income). Are they subject to the Spanish wealth tax? Thank you for sharing your knowledge.

Hi Ed, I am not qualified to give personalized tax advice, so you should book an appointment with our cross-border US/Spain taxation specialist to clarify your position. Per our article on the Spanish tax system, there are two ways you’d qualify as a tax resident in Spain and so be liable for Spanish taxation, including the wealth tax. The Spanish government will generally consider you as a resident for taxation (a fiscal resident) if:

You spend more than 183 days in a calendar year in Spain. This time includes temporary departures from Spain (like a weekend away).

Or

Spain is your main base or center of economic activity. The government could decide you are a resident if you live with your spouse and children in Spain and have a home, investments, or business in Spain, or work for a company in Spain.

https://movingtospain.com/spanish-tax-system/

Regards,

Alastair

Hi there,

Regarding the Spanish Wealth Tax: Most people would say that for NonTaxResidents, (NTR’s), the Wealth Tax is only payable on the SPANISH assets, (not on assets in the NTR’s home country).

We are normally told that the criteria for being a T.R. includes, say, having a Spanish spouse, or staying +183 days, etc…but NOWHERE does it say that owning property in Spain makes one a Spanish T.R.

Your recent reply to Ed Harris on 30-7-24 says that: “The government could decide you are a resident if you live with your spouse and children in Spain, HAVE A HOME, investments, or business in Spain, or work for a company in Spain”. …(“HAVE A HOME” my emphasis).

…Are you really saying that NTR’s (ie a Canadian or USA tax resident, spending -183/365 (hacienda) and -90/183 (Shengen) could, (SIMPLY) IF THEY OWNED A FLAT IN SPAIN, be considered Tax Residents?…. this would mean their entire global assets would be wealth-taxable…Owning a flat or house in Spain is NOT one of the criteria that makes a “foreigner” a TaxRez, AFAIK. And absent any OTHER criteria, (is Spanish spouse/kids, +183 days, etc), simply owning a modest property in Spain (ie -4-500k) should not result in wealth tax on assets/income held OUTside Spain.

Most NTR’s (staying -183 days/no Spanish spouse etc) but owning a second home in Spain, would consider themselves NTR’s. And they would declare only their Spanish assets and income, for tax purposes. You’re saying, “NO; the fact you own a piece of property (can or does) make you a T.R. in Spain”. This conflicts with the government’s own data, (link below).

…could you point to the legislation or other policy statement where this is itemized? Thanks!

https://sede.agenciatributaria.gob.es/Sede/en_gb/no-residentes/impuesto-sobre-patrimonio/exigibilidad-impuesto-sobre-patrimonio-no-residentes.html#:~:text=There%20is%20a%20minimum%20exemption,the%20owner%20on%20said%20date%20.

Hi Peter – As always, I am not a qualified tax expert, and any advice is general in nature. You are 100% correct that simply owning a property in Spain will not automatically make you a tax resident. I’ve made a minor amendment to the original comment for clarity – the key is that your financial base is in Spain (and owning a home plus other indicators could make this case), which could make you a tax resident in Spain. All the best, Alastair

Hi, I was wondering how come you did not mention the “Beckham Law” status that an expat could have for the first 6 years in Spain, paying no wealth tax on assets outside the country? Correct?

Hi Nuria that is an oversight by us. Thank you for pointing it out. I have now added a link to our detailed article on the Beckham Law, which is indeed a way to avoid paying Wealth Tax in Spain. Thansk, Alastair

This article fails to mention the new “solidarity wealth tax” that applies to those living in Madrid and Andalucía.

It only applies to those with over €3M in assets, but it now means those territories are not always zero wealth tax.

This article needs updating.

Hi – there is a paragraph (see the table of contents) and an FAQ that refers to the Solidarity tax (impuesto de solidaridad a las grandes fortunas). I’ve just updated this with a qualification for the Autonomous Regions of the Basque Country and Navarra, which operate under a different tax regime. Thnaks, Alastair

Very nice page!

I see that if I were to reside i Andalusía, there’s no wealth tax. None whatsoever? Or none to Andalusia, but still to the national government?

I ask, because in the US, there is always file a federal tax, in addition to any state tax.

Hi Sean. There is an effective 0% regional wealth tax in Andalusia, but you’ll still need to pay the Solidarity tax to the Spanish government if you have assets over that threshold. Regards, Alastair

Hi. Thinking of moving to Spain in 18 months

Irish husband with uk wife. Have an off shore account which we are hoping to draw on to provide monthly payment to us. What are the tax implications. We have a small apartment in Spain and a property in france.

Hi Derrick. It depends on the value of the account, the type of account, and where you intend to move in Spain. Given the complexity, it is tough for us to give you a direct answer. Our tax specialist partner, Louis, will provide you with a much more accurate answer. https://movingtospain.com/services/tax-advice-spain/ All the best, Alastair

Is life insurance considered as part of the wealth asset?

Hi Walid. In most cases an life insurance policy would not be declared as an asset in the Modelo 720 and so not subject to wealth tax in Spain. All the best, Alastair

Hi Alastair,

Does an annuitized annuity income qualify four the wealth tax?

Meaning, if you put 1 million into an annuity and then annuitize it for monthly lifelong income does Spain tax that income. Once annuitized the money is owned by the insurance company in exchange for lifelong monthly income. So technically they own the 1 million. Is that counted as an asset?

Is the monthly income taxed?

Is the monthly Social Security income taxed?

What if both incomes streams are above 10k a month?

If no wealth or solidarity tax is owed, then is there an INCOME TAX?

Thank you for your wealth of information.

Hi Carmen. For this detail I’d suggest speaking with our Spanish tax specialist partner. Any advice I can five is only general in nature but Louis will accurately map your potential tax liabilities and walk you through some strategies to manage this. All the best, Alastair